From Fragmented Data to AI-Ready Customer Outcomes: A Master Data Blueprint for Banks

Overcome fragmented, siloed customer data challenges and reach AI ambitions with our practical blueprint for placing master data at the centre of your bank to support priorities across operations, compliance, and growth.

In our previous blog post, we explored why a pragmatic master data approach is essential for delivering trusted AI outcomes and how banks are modernizing their digital and AI enablement through key master data management services. Organizations require an accurate, steady delivery of master data before they can gain value from AI, including a means to identify consistent entities across producer systems and a mechanism to share data across consumer channels, both operational and analytical.

But what does this look like in practice, when applied to real, day-to-day banking priorities?

A practical blueprint for leveraging master data for AI

Banks need a clear blueprint to leverage master data in support of AI, wherein it is no longer viewed as a data management exercise, but rather as the connective tissue between operations, regulation, growth, and AI. Creating this blueprint is what we'll talk about in this blog post.

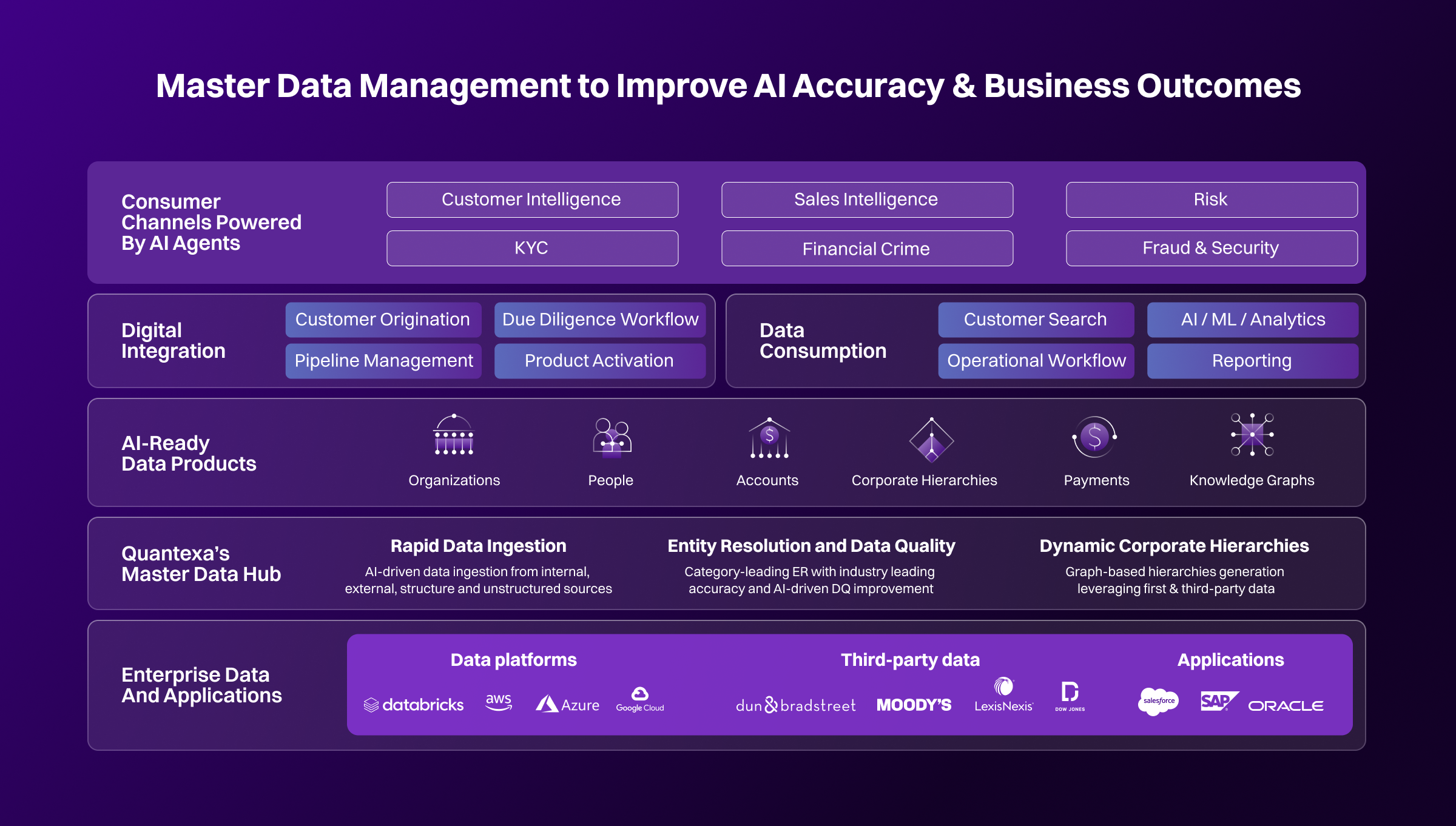

Banks that have done this well integrate producer systems and consumer channels with master data management at the core. The following platform blueprint brings these producers' systems, both internal and external data, connected through a master data hub, serving AI-ready data products for various business consumer channels.

In practice, this approach unlocks value across the bank. Using high‑accuracy entity resolution and graph generation, banks can create:

A consistent customer identity across lines of business

Integrated customer master with operational, analytical, and AI solutions

Explainable linkages that regulators and auditors can trust

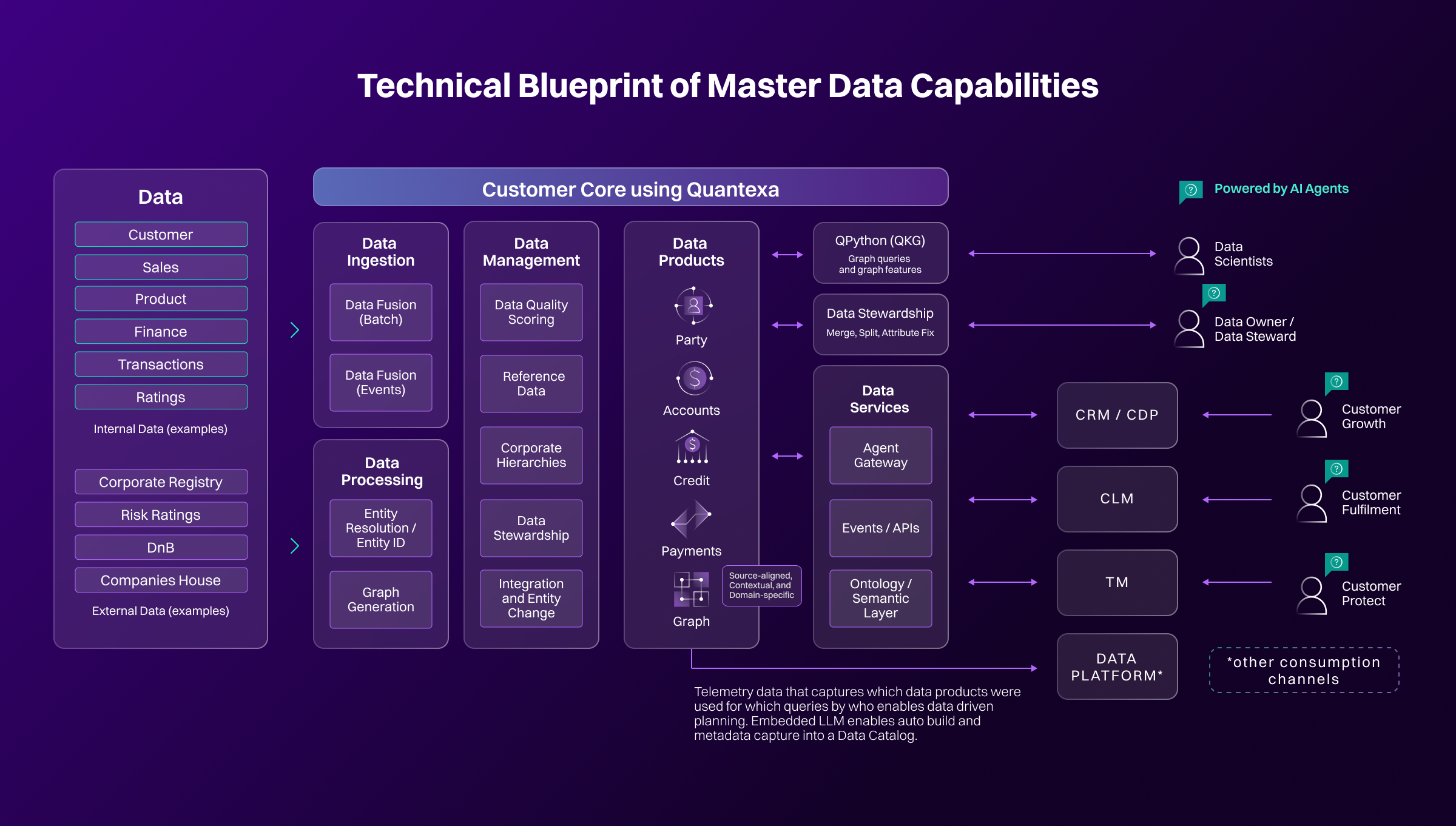

A 'customer core' at the center

A bank's customer data cannot be viewed as a static record, or even a periodically refreshing one. Rather, it should be seen in its totality as a living entity, enriched with relationship context, ownership structures, hierarchies, and behavioral signals that update continuously.

Successful AI implementation in banking is only possible with contextual and trusted entity data: knowing confidently who your customers are, how they're connected, and ensuring that picture remains clear and accurate over time. This is why the resolved customer and counterparty core must exist at the center of the banking blueprint.

For most banks, the KYC process is the starting point for everything from customer relationships to regulatory compliance to risk assessments. However, the desired outcomes of this process are impeded by issues such as slow manual onboarding, periodic reviews, and fragmented customer data. This results in delays, poor customer experience, increased costs, and risks that surface too late.

With a resolved customer core, banks can automate the analysis of complex ownership structures and relationships. Beneficial owners are identified more reliably, and due diligence packages can be pre-populated. Analysts can spend less time reconciling data and more time investigating risk.

Leveraging a resolved customer and counterparty core also necessitates a shift from periodic, calendar-driven reviews to event-driven risk assessment. Instead of reassessing customers on a designated date every two, five, or ten years, reviews are triggered when something meaningful changes: say, a change in ownership, unusual customer behavior, or a link to an emerging risk signal.

From compliance gaps to sustainable growth

Fragmented customer data doesn't just create operational friction; it becomes a balance-sheet issue. When customer and counterparty records are inconsistent, banks can't accurately aggregate total risk exposure. Connections between customers are overlooked, concentration risk is underestimated, and risk-weighted assets are inflated because exposures can't be reliably consolidated. Because of a lack of clarity around their customer data, many institutions fall short of complying with regulations such as BCBS239.

Banks that resolve their entity data consistently find that their RWA calculations improve, not because the risks have changed, but because their data shows an accurate picture. This allows them to free up capital that would otherwise be tied up to hedge against financial losses.

But trusted master data is about more than risk detection; it also fosters growth. With a resolved, contextual customer view, relationship managers gain a complete picture of their clients: products held, organizational structures, connections to other parties, and behavioral signals across channels. This enables more informed conversations with customers, better prioritization of their needs, and more relevant products and services.

Importantly, this doesn't require building a separate "sales data mart". Rather, it necessitates a departure from an approach in which data is siloed. The same master data used for KYC and risk aggregation is surfaced through APIs into CRM and front-line tools, ensuring consistency across the organization.

Understanding the integration layer

None of this works in isolation. The master data hub sits at the center of a broader ecosystem, integrating internal and external platforms that generate data, then delivering it to downstream channels that consume it.

Here's how it works:

Upstream, it ingests data from digital front-door channels, customer acquisition platforms, origination systems, and the enterprise or customer data platform.

Downstream, it publishes enriched, trusted data products to the tools where decisions are made: CRM and sales tools, KYC workflow platforms, risk and regulatory systems, business intelligence, and, increasingly, AI agents that need reliable context to act autonomously.

Integration evolves as trust grows. Early on, data typically flows in, and resolved entities flow out. Over time, corrected and enriched records are pushed back into origination and CRM systems, closing the loop and improving data quality at source.

Grounding AI workflows in trusted data

As banks increasingly rely on generative and agentic AI-driven tools, the importance of a trusted contextual data foundation only increases. Without this, outputs are inconsistent or suspect, and decisions become difficult to explain, defend, or unwind.

A master data hub provides the grounding layer AI needs. When AI retrieves information from resolved customer and account entities, responses are consistent across users and channels.

Relationship context reduces hallucinations and enables accurate processes. Decisions are explainable and auditable.

AI moves successfully from pilot to production when it is embedded in real banking workflows and supported by trusted data. Only then can real value be captured from AI transformation.

Looking ahead

This banking blueprint is not about building separate solutions for operations, regulation, and growth. It's about recognizing that the AI-driven processes that are being implemented across all these verticals fundamentally depend on the same contextual, trusted entity data: knowing who your customers are, how they're connected, and keeping that picture accurate.

By placing master data at the center of the bank and delivering it incrementally through reusable data products, banks can support today's priorities while creating a durable foundation for AI. And most importantly, they don't need to wait for all their data to be perfect. If they can identify consistent entities and integrate data across various departments or joined organizations, they can begin today.

We recommend that banks start with one outcome-led capability and one data product, then prove it works before scaling and addressing any issues as they go.

Organizations that can successfully leverage MDM will have a structural advantage: a trusted data core that is AI-ready and primed to support scaling and organizational growth. Every decision will be more accurate, more explainable, and more trusted.

The future of banking belongs to those who build on trust. When banks place their customer data core at the center, they don't just solve today's regulatory compliance or growth challenges; they unlock tomorrow's AI capabilities, and with them, a true competitive advantage.

Loading...

Loading...