Smarter Underwriting Decisions in a Soft Market

In a softer market, speed and context matter more than ever. The ability to act on the right risks first can define underwriting success.

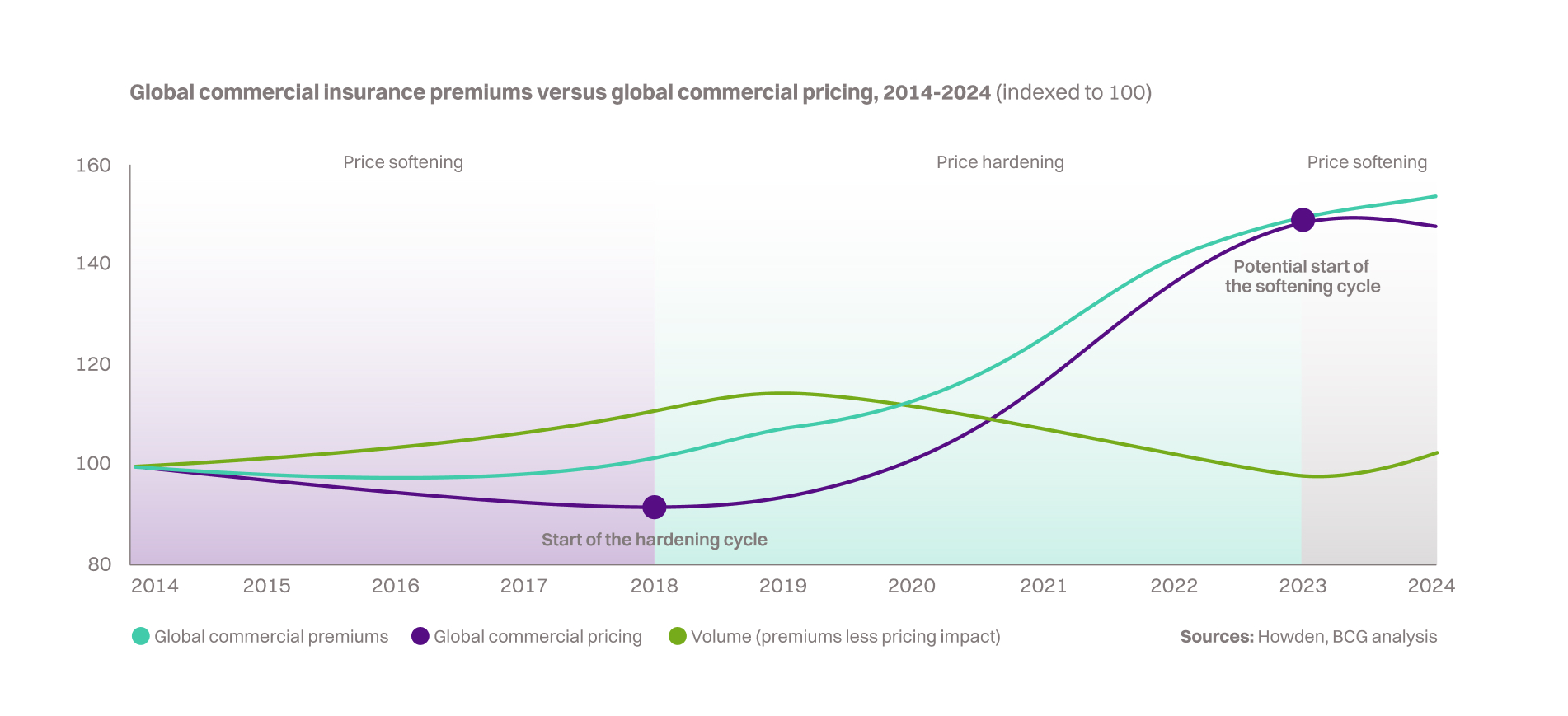

A soft insurance market is emerging, as seen in the deceleration of premium increases. For example, U.S. commercial insurance rates rose only 3.8% in Q2 and Q3 2025, down from 5.3% in Q1 2025 and 5.6% in Q4 2024 (WTW). The trend varies by segment: large commercial lines are softening more than middle-market, and some lines like workers' compensation and cyber insurance have seen actual price decreases. Commercial property saw its first price drop after several quarters of slowing growth (BCG).

The challenge: This softening market presents a paradox. To offset lower prices, insurers must grow their market share. However, the accompanying surge in submission volume often brings lower-quality applications and incomplete data. Underwriters, already spending 30-40% of their time on administrative tasks like re-keying information, become inundated (McKinsey). In this high-pressure environment, even a few seconds' delay in responding to a quote can dramatically reduce the chances of winning business by over 90% (Moody’s).

The core challenge is clear. Insurers need to process submissions faster and smarter, not just in greater numbers. Success in a soft market belongs to those who can quote the right risks quickly and decline the wrong ones early. BCG’s 2025 analysis echoes that as rates soften, carriers must improve underwriting efficiency and leverage technology to protect margins. This is a task perfectly suited for Decision Intelligence.

A new approach to proactive underwriting and decision intelligence

Traditional underwriting is often reactive. Un underwriter manually reviews a broker’s submission, then requests missing information, and eventually quotes. Proactive underwriting, powered by Decision Intelligence (DI), flips this script.

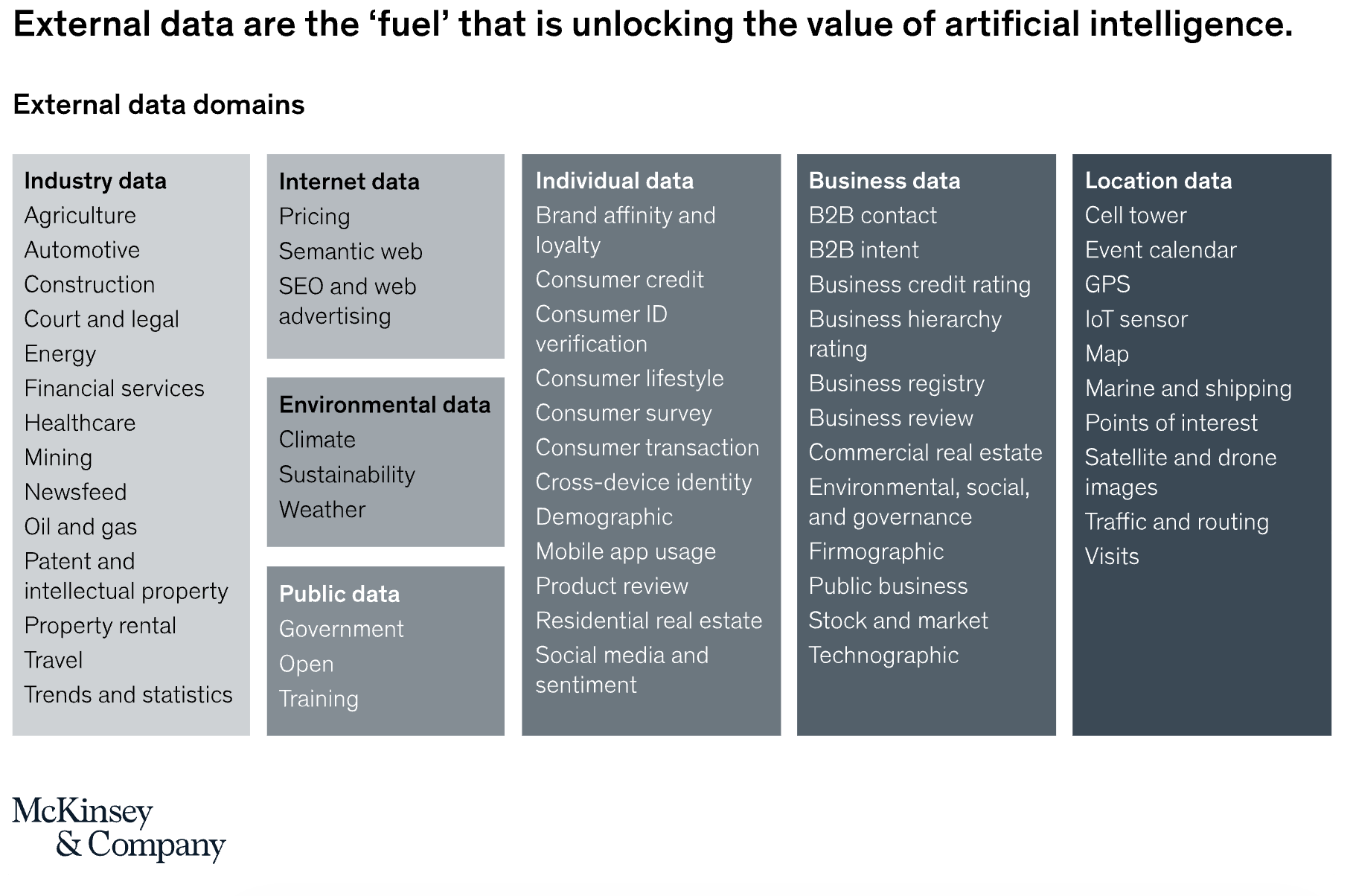

The moment a submission comes in, the insurer’s system enriches, analyzes, and triages it before an underwriter even touches it. DI platforms unify an insurer's internal data (e.g., policies, claims) with a vast array of external sources (e.g., financial records, firmographics, geospatial risk data, loss benchmarks). As McKinsey indicated, external data are the “fuel” that is unlocking the value of AI. By connecting both internal and external data, DI creates a complete, 360-degree profile of the risk at intake. Instead of wrestling with fragmented data, underwriters are presented with connected, contextual insights.

Decision Intelligence doesn’t replace underwriters. It augments them, providing real-time analytical assessments so underwriters can make faster, more informed decisions. For example, AI-driven triage can automatically classify and prioritize submissions. A high-potential submission matches the insurer’s target profile (e.g. desired industry, within risk appetite and no red flags), can be fast-tracked for an immediate quote or even straight-through processing. Conversely, a submission that is clearly out of appetite can be flagged for a quick decline, saving valuable underwriter time. The result is that underwriters only spend time on viable, enriched opportunities, improving productivity and hit ratios.

Key components of proactive DI-enabled underwriting:

Rich data at intake: DI platforms use entity resolution to link data (e.g., recognizing “ACME Inc.” is the same as “Acme Corporation” in another system) and pull in external insights, such as hierarchy, credit scores, news. Underwriters start with a fuller picture of the risk instead of chasing details.

Intelligent triage: Rather than a FIFO queue or gut feel, submissions can be algorithmically scored and routed. Triage analytics can weigh factors like appetite fit, premium potential, likelihood to bind, and data completeness. For example, a small commercial package submission with all key info present and falling squarely in appetite might get a high score – signaling “quote this fast.” Another submission with missing loss runs or in a tougher class (say, a habitational risk outside appetite) scores low – signaling “low priority or decline.” If a submission is straightforward (low complexity, low risk), DI can enable straight-through processing, automatically pricing and generating a quote within minutes or even seconds, subject to underwriter review.

Risk assessment and pricing insight: By analyzing submissions against historical data and benchmarks, DI provides underwriters with data-driven risk scores and pricing recommendations. Importantly, Decision Intelligence emphasizes explainable AI – underwriters (and regulators) can see why a model flags a risk, using transparent features like past loss frequency, OSHA incidents, or network connections to known loss-makers. This ensures consistency and compliance in underwriting decisions.

Continuous learning: A proactive approach doesn’t end at quote issuance. Feeding outcomes such as which quotes turned into binds, which turned into profitable accounts vs. losses, back into the model, overtime trains the model to sharpen triage and pricing recommendations. As Deloitte observes in 2025, 82% of carriers plan to adopt “agentic AI” in the next 3 years to dynamically handle tasks like this across underwriting and distribution.

Tangible outcomes of proactive DI underwriting

By embedding Decision Intelligence into the underwriting process, insurers can realize tangible improvements in both efficiency and effectiveness. Industry reports show that digitized, analytics-driven underwriting can lead to:

3-5 point loss ratio improvements (McKinsey)

10-15% new premium uplift (McKinsey)

5-10% better retention (McKinsey)

30% productivity gain (Accenture)

Case study: Underwriting transformation at a U.S. Carrier

A top 10 U.S. commercial insurer faced soft-market headwinds and an overwhelming volume of submissions. Data was spread across 20+ lines of business and over 10 million customers. Quote turnaround takes weeks to gather and validate information, and underwriters were burning time on data gathering, leading to missed opportunities and uneven risk decisions.

Solution: The insurer implemented a Decision Intelligence platform by Quantexa, featuring Entity Resolution, to create a single, unified view across diverse lines of business, achieving remarkable transformation:

policy issuance time cut from weeks to hours, 10-30x faster

75% automation in pre-population and analytics modeling, reducing manual effort

98% entity match accuracy (up from ~60%), empowering analytics and data science teams

open-box configurations and explainable AI models delivered, ensuring clear decision-making processes and regulatory compliance

new high-value cross-sell opportunities unlocked by connecting data across commercial lines, group benefits, and global specialty businesses

The results were transformative. According to the Chief Data Officer: "Underwriting is having great success. Work that previously took over 40 hours across two weeks can now be done in seconds by this system and minutes by the team."

Quick steps to start leveraging DI for the soft market

1. Assess current data quality: Review your submission intake process and identify gaps in data completeness and context.

2. Integrate internal and external data: Connect internal, such as policy, claims, and third-party data sources to create unified client profiles.

3. Adopt automation: Implement Decision Intelligence solutions (such as Quantexa) to automate data enrichment, triage, and risk scoring.

4. Monitor and refine: Continuously feed outcomes back into DI systems to improve triage, pricing, and underwriting guidelines.

Winning in the soft market with DI-powered underwriting

As the commercial insurance market softens, the winners will be those who adapt the quickest. Proactive underwriting powered by Decision Intelligence allows insurers to triage submissions intelligently, enrich risk profiles instantly, and automate routine work. By equipping underwriters with DI, you empower them to say "yes" to good risks faster and "no" to bad ones sooner. This turns underwriting from a reactive necessity into a powerful strategic advantage.

Ready to transform your underwriting with Decision Intelligence? Request a demo to see how Quantexa’s platform can help your team win in the soft market.

Loading...

Loading...