A Guide to Detecting and Combating Bank Fraud

Your essential guide to detecting and combatting bank fraud: what it is, the different types, how to detect bank fraud, and measures to prevent it. We also dive into the key components of a fraud detection system, and some examples.

Bank fraud is evolving at a rapid pace, fueled by digital transformation and increasingly sophisticated criminal tactics, like AI being used to generate deepfakes and synthetic ideas at scale, and automation of money mule recruitment. From account takeovers and phishing schemes to insider threats and synthetic identities, the landscape of financial crime is more complex than ever before.

Financial institutions face constant pressure to safeguard customer assets while maintaining smooth, trustworthy operations – and the consequences of failure can be devastating, both financially and reputationally.

This guide explores how banks can detect and combat fraud in all its forms. It examines the key techniques used by fraudsters, outlines the challenges which financial institutions are currently facing, and highlights the tools and technologies available to strengthen defenses.

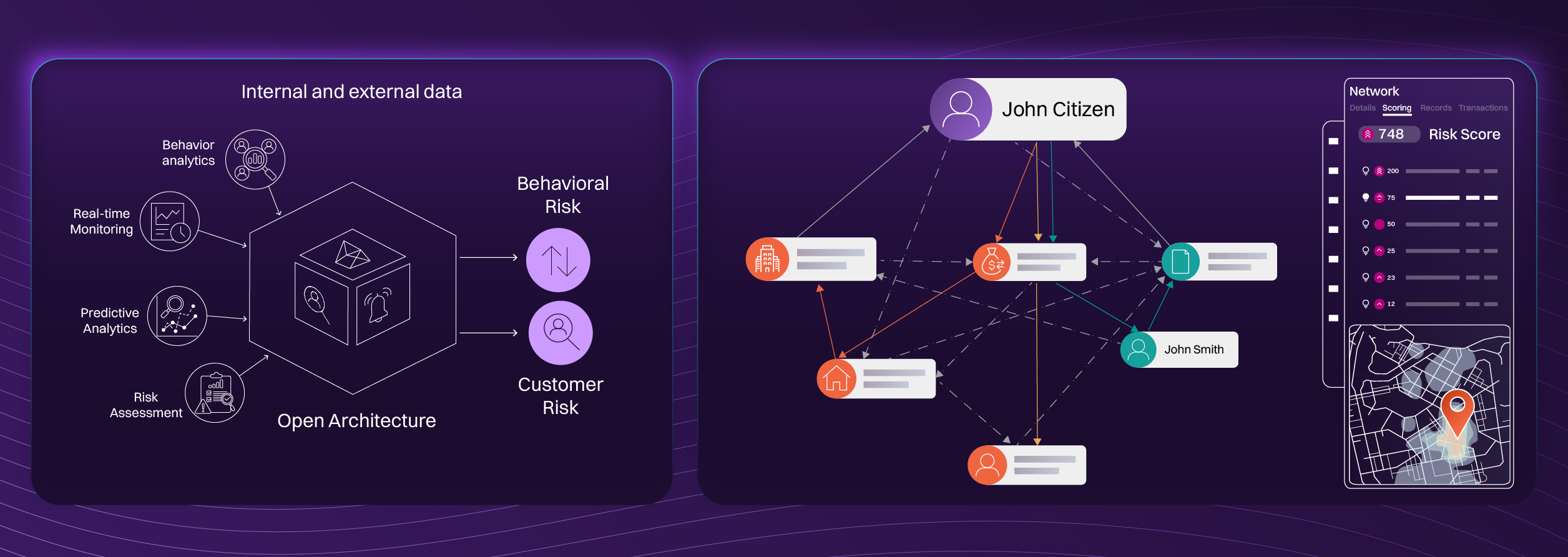

What is bank fraud detection?

Bank fraud detection is the practice of identifying, monitoring, and preventing unauthorized financial activity through a blend of advanced technology, data analytics, and human intelligence. It requires the continuous monitoring and analysis of transaction data, customer behavior, and other indicators to uncover irregular patterns that may suggest criminal activity – from identity theft and account takeovers to complex money laundering schemes.

By combining automation with expert oversight, banks can detect threats earlier, respond faster, and maintain trust in an increasingly digital financial landscape. Ultimately, effective fraud prevention, detection and investigation safeguards both institutions and customers from financial loss and long-term reputational harm.

How does fraud detection work in banks?

Banks use a range of tools and techniques to detect fraud, analyzing transaction data and customer behaviour to flag unusual or unauthorized activity. A combination of technology and expert input can identify potential threats early and take swift action to protect accounts and assets. Some of the most proficient ways to detect fraud are:

Behavioral analysis

Financial institutions build individualized customer profiles by tracking typical spending behavior, transaction frequency, and interactions with devices and platforms. Unusual activity that strays from these established patterns can trigger warnings for potential fraud. For example, a customer who usually makes occasional purchases might be flagged if they suddenly conduct numerous transactions in a short period, prompting further investigation.

Pattern recognition

Banks examine past transaction records to detect irregularities that could signal fraud. An account showing unexpected high-value transfers from a previously unused device or location may be highlighted for further review, helping institutions respond quickly to potential threats.

Two-factor authentication (2FA)

Adding extra security measures, like delivering a one-time verification code to a customer’s mobile device, can significantly reduce the risk of unauthorized account access. This is an increasingly common option for customers across a number of different platforms.

Data analysis

Banks can detect potential fraud by examining data from multiple channels, such as transaction records, social media activity, and online reviews, to uncover suspicious patterns and behaviors. Deep dives into customer data insights are one of the most powerful weapons in a financial organization's arsenal.

Machine learning (ML) and Artificial Intelligence (AI)

Cutting-edge AI and sophisticated algorithms analyze vast datasets to detect subtle patterns that may elude human observation. As these systems process more information, they refine their models, continuously enhancing their ability to identify and predict fraudulent activity with greater precision.

Geographic location data

Financial institutions leverage geolocation information from mobile devices and IP addresses to confirm a customer’s location during transactions. Activity originating from an unexpected or unusual location can trigger alerts, prompting further verification to prevent potential fraud.

Real-time monitoring

Fraud detection platforms monitor transactions and account activity as they occur, instantly identifying irregularities and raising alerts for immediate review and investigation.

What are the challenges for banks to detect and combat fraud

Meeting regulatory and anti-fraud obligations remains a major hurdle for many financial institutions. Falling short of compliance requirements can lead to significant penalties, reputational harm, and a decline in customer confidence. Staying aligned with ever-changing regulations and emerging fraud risks is essential, as criminals constantly adapt their methods to exploit system gaps.

Beyond this, providers must also contend with challenges such as:

The evolving nature of fraud schemes

Fraudsters continually devise innovative ways to exploit weaknesses within the banking sector, often using advanced technologies, including biometric spoofing, to circumvent standard security protocols. In response, banks must remain vigilant, proactively enhancing their defenses and deploying comprehensive systems designed to detect, prevent, and mitigate all forms of financial attacks.

Mitigating pain points for customers

Striking the right balance between strong security and a smooth customer experience is a persistent challenge for banks. While rigorous measures can help prevent fraud, they can also frustrate customers and slow down transactions. If security protocols are overly cumbersome, banks risk damaging the user experience, which can lead to client dissatisfaction and, ultimately, customer attrition.

The increasing commonality of fraud

Banks track thousands of potentially fraudulent activities every day. Fraudsters employ a wide range of tactics to deceive both businesses and individuals into approving unauthorized transactions. Managing this constant influx of threats across a large customer base demands highly sophisticated systems and agile processes, enabling banks to detect, respond to, and prevent fraud effectively in real time.

Financial identity factors

When criminals gain access to customers’ login details or sensitive account information, they can take control of accounts and carry out unauthorized transactions. This type of fraud is particularly damaging because it directly threatens financial assets rather than just personal data. Banks must address this risk through stronger security measures, such as multi-factor authentication, alongside educating customers on safe practices for managing their account information.

Organizational buy-in and policies

Effective fraud prevention depends on strong organizational support and clear internal policies. When leadership champions security measures and employees understand their roles, the organization can respond swiftly to threats, enforce consistent practices, and protect both financial assets and customer trust.

Banks checklist to preventing fraud

Institutions must be prepared to detect and combat fraud at every potential avenue. That means having a series of measures in place that adhere to the best practices of dealing with fraud prevention. These span a number of areas within an organization, including process management and preventative controls. Some of the most important factors to check off are:

Internal processes

The establishment of fraud detection practices.

The assignment of core responsibilities to individuals.

Regular audits to assess if existing processes are working.

Ongoing training and awareness programs for employees.

Strict termination procedures for employee access removal.

Employee reporting avenues.

Online and technical security controls

Use unique passwords for each account and manage them securely with a password manager.

Activate two-factor or multi-step authentication wherever possible.

Update operating systems, antivirus programs, and security tools regularly.

Avoid using business computers for personal activities.

Exercise caution when opening attachments or downloading files.

Frequently back up important information to secure, offsite, or cloud-based locations.

Encrypt confidential files stored on local drives or portable devices.

Activate alerts for unusual account activity or large transactions.

Enable fraud prevention features like Positive Pay.

Never share sensitive details over unsecured email.

Use encrypted channels for confidential correspondence.

Paper check controls

Keep critical papers in locked, fire-resistant cabinets or safes, and shred any documents before disposal.

Use checks with built-in security features, store blank checks securely, and conduct regular audits to prevent misuse.

Limit entry to sensitive files and secure mechanical signature plates.

Never leave confidential information exposed on desks or printers.

Use high-quality shredders or professional shredding services for disposal.

Types of fraud detected in banks

Fraud can take a variety of shapes. The continued advancement of technology, coupled with inventive and evolving approaches from fraudsters themselves, means that a wide variety of common fraud types now need to be managed by banks on a daily basis. Here are some of the most common:

Loan fraud

Loan fraud takes place when individuals provide false or misleading information to obtain credit or loans, often with no intention of repayment. This includes falsified income, employment details, or stolen identities. Banks mitigate risk through thorough application verification, credit checks, identity authentication, and fraud detection systems to prevent financial loss and abuse.

Insider fraud

Insider fraud involves employees or trusted individuals within an organization exploiting their access to commit financial crimes, such as embezzlement, unauthorized transfers, or data manipulation. It poses a significant risk due to insider knowledge. Prevention relies on internal controls, access monitoring, segregation of duties, and fostering a culture of accountability and oversight.

Phishing

Phishing is a fraudulent technique where attackers impersonate trusted organizations via emails, messages, or websites to steal sensitive information like passwords, account numbers, or personal data. This information is then used for financial fraud or identity theft. Prevention relies on customer education, email filtering, and robust fraud detection systems.

Online banking fraud

This kind of attack happens when criminals gain unauthorized access to a customer’s bank account through phishing, malware, or compromised credentials. They can initiate fraudulent transfers, payments, or withdrawals. Banks combat this threat with multi-factor authentication, real-time transaction monitoring, encryption, and educating customers about safe online banking practices.

Money laundering

Money laundering is the process of concealing the origins of illegally obtained funds to make them appear legitimate. Criminals often use complex transactions, shell companies, or international transfers. Financial institutions combat money laundering through transaction monitoring, know your customer (KYC) procedures, suspicious activity reporting, and regulatory compliance to prevent illegal funds from entering the financial system.

Identify theft

Identity theft happens when a fraudster steals personal information, such as Social Security numbers or account details, to impersonate someone else. This can lead to unauthorized transactions, account takeovers, or fraudulent credit applications. Banks combat it through strong authentication, monitoring unusual activity, and educating customers on protecting their personal information.

Credit and debit card fraud

This type of fraud occurs when unauthorized individuals use stolen or compromised card details to make purchases or withdraw funds. This can involve physical theft of cards, skimming devices, phishing scams, or online data breaches.

The consequences include financial losses for both customers and banks, along with potential reputational damage. Preventative measures include real-time transaction monitoring, secure payment systems, multi-factor authentication, and educating customers on safe card usage.

Check fraud

Check fraud involves the use of counterfeit, altered, or stolen cheques to illegally withdraw funds or make payments. Common tactics include forging signatures, altering amounts, or depositing fake checks. Banks prevent this through verification processes, positive pay systems, and transaction monitoring to detect and stop suspicious cheque activity.

Create context to counter the rise of fraud

What are the benefits of bank fraud detection?

There are a plethora of reasons why banks can benefit from a strong fraud detection system. Robust banking fraud detection safeguards customers’ funds and sensitive information, reinforces confidence in financial institutions, and minimizes losses from fraudulent activity. Achieving this requires a continuous effort that blends advanced technology, thorough data analysis, and skilled human oversight to anticipate and respond to increasingly sophisticated fraud schemes.

Some of the most effective reasons why financial organizations should invest in these kinds of measures are:

Financial loss prevention and mitigation

Criminal activities like account takeovers, credit card misuse, and other unauthorized transactions can lead to substantial financial damage for both banks and their customers. Advanced fraud detection systems play a crucial role in minimizing these losses by swiftly identifying suspicious behavior and blocking fraudulent activity before it causes harm.

AML prevention

Fraud detection systems go beyond spotting isolated incidents. They also help uncover broader criminal activities such as money laundering and illicit fund movements. By identifying suspicious patterns across transactions, these systems play a vital role in safeguarding the financial ecosystem and upholding the integrity of regulated banking operations.

Early detection

Early detection enables banks to act quickly and contain potential threats before they escalate. By identifying suspicious activity in its initial stages, institutions can minimize financial loss, prevent further compromise, and protect both customer accounts and the wider banking network from cascading fraud impacts.

Legal and regulatory compliance

Banks operate under strict regulatory frameworks that require them to protect customer information and prevent financial misconduct. Implementing advanced fraud detection systems not only strengthens security but also ensures compliance with these legal standards, helping institutions avoid penalties, maintain regulatory trust, and uphold their reputational integrity.

Reputation management

Customers rely on banks to safeguard their money and personal information. When fraud goes undetected, that trust can quickly erode, damaging the institution’s credibility and customer relationships. Proactive fraud prevention is therefore vital not just for protecting assets, but for preserving reputation, confidence, and long-term customer loyalty.

Minimization of false positives

Detecting fraud effectively requires precision as much as vigilance. Overzealous systems that flag legitimate transactions can frustrate customers and disrupt business, as well as overwhelm alert analysts and increase costs. Modern fraud detection tools use advanced analytics and adaptive algorithms to minimize false positives, ensuring that genuine transactions proceed smoothly while real threats are swiftly identified and stopped.

Bank fraud trends in 2026

An intrinsic element of financial fraud is its ability to constantly adapt and evolve. Just as institutions believe they might have fully mastered preventative tactics with one fraud pathway, new avenues emerge to pose fresh challenges. One of the best ways to continue the fight against fraud is to understand what tactics are being employed, and what new steps criminals are taking to gain illicit access to funds.

In impersonation scams, fraudsters pose as trusted individuals, such as company executives, customers, or bank representatives, to manipulate targets into approving unauthorized transactions or divulging sensitive information. These attacks often rely on urgency, authority, or familiarity to pressure victims, making them highly effective. Prevention relies on verification protocols, employee training, and clear communication channels.

Examples:

Customer impersonation

CEO fraud

Bank employee impersonation

Family and friend impersonation

With advances in AI, criminals can create highly realistic audio and video deepfakes that impersonate trusted individuals, such as company executives or clients. These synthetic interactions can trick employees into authorizing fraudulent transactions or revealing confidential information. Combating this requires awareness, verification protocols, and technology capable of detecting manipulated media.

Examples:

Voice-cloning technology

Deepfake video scams

AI-specific impersonation scams

Synthetic stolen identity scams

Stolen identify scams

Many fraud defenses rely heavily on consumers, using generic warnings or scam-awareness messages. These often fail to change behavior, create friction, and leave blind spots that fraudsters can exploit. Social engineering attacks take advantage of human psychology, allowing criminals to bypass technical safeguards and manipulate victims.

Examples:

Authorized Push Payment (APP) Fraud

Romance scams

Investment scams

Online marketplace scams

The importance of AI and ML in bank fraud detection

AI and ML have already had a monumental impact on the financial sector. Automation has been a useful asset for organizations who are looking to streamline and optimize their internal processes, without the need to inject excess funding into these areas. This has been true in fraud detection already, with some of the core functions of these tools being:

Anomaly detection and isolation

AI technologies excel in detecting complex patterns across large datasets, making them invaluable for fraud prevention. Graph Neural Networks (GNNs), in particular, are designed to analyze interconnected data commonly found in banking. By processing billions of data points, GNNs can uncover hidden links and detect sophisticated fraud schemes with exceptional precision.

Risk scoring and profiles

AI and machine learning models use weighted data to evaluate probabilities and determine the most likely outcomes of various actions. By analyzing factors such as transaction size, frequency, location, and historical behavior, they can accurately assess risk levels. This enables banks to detect suspicious transactions and evaluate creditworthiness, reducing exposure to fraudulent applicants.

Deep network analysis

Machine-learning techniques such as graph analysis enable banks to map relationships between customers, accounts, and transactions. By identifying unusual links or tightly connected clusters, these systems can reveal hidden networks of fraudsters, uncovering coordinated schemes that might otherwise go undetected through traditional rule-based monitoring.

Human workforce cohesion

Human fraud analysts can now leverage LLM-powered AI assistants to enhance efficiency and accuracy. These tools allow users to interact with complex systems through natural language, quickly querying vast datasets or referencing intricate policy documents. This streamlines investigations, reduces manual workload, and enables faster, more informed decision-making in fraud prevention.

What to look for when selecting bank fraud detection software

Selecting the right fraud management software is critical for an organization’s effectiveness. To ensure the chosen tools meet your requirements, it’s important to evaluate their capabilities against your specific needs. This decision-making process can be structured into three key stages, each focusing on core factors that determine whether a solution can support your operational goals and scale with your business.

Work out business needs

First, clearly define the objectives and performance metrics you expect the software to deliver. This includes considerations such as:

Determine key fraud risks. Identify the fraud scenarios most likely to impact your business, such as unauthorized payments, account compromises, or identity misuse.

Examine transaction capacity. Review both current and anticipated transaction volumes to ensure the system can scale effectively with your operations.

Consider team requirements. Decide if your staff can manage a feature-rich platform independently or if a solution with vendor-managed support would be more suitable.

Assess features of the software

After establishing the desired outcomes and metrics, the next step is to evaluate the specific features the software offers. Key aspects to consider may include:

Intelligent analytics and AI. Seek solutions that leverage machine learning to detect emerging fraud trends and adapt as tactics evolve.

Growth-ready scalability. Confirm the system can handle increasing transaction volumes without sacrificing detection accuracy.

Seamless integration. Ensure compatibility with your existing systems, including e-commerce platforms, CRMs, and payment processors.

Flexible configuration. Choose software that allows rule adjustments and risk parameter customization to fit your business model.

Accurate detection. Favor solutions designed to minimize false positives, reducing disruption to legitimate customer transactions.

Think about additional support from the service provider

After selecting a software platform, ensuring reliable ongoing support is essential. It’s important to clarify what assistance the provider offers. Key considerations are:

Provider credibility. Investigate the vendor’s track record, reviewing client testimonials and case studies to assess reliability and effectiveness.

Ongoing support. Select a provider that delivers continuous assistance, regular updates, and a transparent maintenance strategy.

Regulatory compliance. Verify that the software supports adherence to relevant industry standards and data protection regulations.

Value for money. Evaluate the cost relative to the protection offered, ensuring the solution delivers robust security without unnecessary overspending.

By following these steps and utilizing Quantexa’s advanced analytics and machine learning capabilities, you can enhance your organization’s ability to detect and prevent fraud more effectively. Remember to request a demo and consult with Quantexa’s experts to tailor the implementation to your specific needs and challenges.

FAQs

How do banks investigate fraud?

Banks investigate fraud through a combination of technology, data analysis, and human expertise. They begin by monitoring transactions and account activity in real time, flagging unusual behavior or anomalies. Advanced analytics and machine learning help identify patterns indicative of fraud, while investigators review suspicious cases, gather evidence, and collaborate with law enforcement or regulatory bodies to confirm incidents and take appropriate action. This multi-layered approach ensures timely detection, accurate assessment, and effective mitigation of fraudulent activity.

Is there fraud protection on bank accounts?

Yes, U.S. bank accounts are protected against fraud through a combination of regulatory safeguards, bank policies, and advanced security measures. Financial institutions implement around-the-clock monitoring to detect unusual activity, while multi-layered authentication – such as passwords, PINs, and biometric verification – helps prevent unauthorized access. Many debit and credit cards also include consumer protections, like zero-liability policies, ensuring account holders are not financially responsible for fraudulent transactions.

Key measures include:

Continuous monitoring. Banks track transactions and account changes in real time to spot suspicious activity.

Advanced security features. Passwords, PINs, and biometric checks secure online and mobile banking.

Multi-layered authentication. Additional safeguards prevent unauthorized access.

Alerts and verification. Banks notify customers of unusual activity, though they will never request sensitive information like passwords or PINs over the phone.

How can I protect my bank account from fraud?

Protecting your bank account from fraud requires a combination of vigilance, good habits, and the use of available security tools. Start by creating strong, unique passwords for online and mobile banking, and enable multi-factor authentication whenever possible. Monitor your accounts regularly for unusual transactions, and set up alerts for large or suspicious activity. Keep your devices secure with updated software, antivirus protection, and cautious use of public Wi-Fi. Finally, never share sensitive information such as PINs, passwords, or account numbers, and be wary of unsolicited communications requesting personal details.

Do banks refund money if scammed?

In many cases, banks may refund money lost to scams, but this depends on the circumstances and the type of fraud. U.S. regulations and card network policies often protect consumers against unauthorized transactions, especially if the fraud is reported promptly. Banks typically investigate the incident to determine liability. However, if the account holder is found to have been negligent, such as sharing passwords or PINs, reimbursement may be limited or denied. Reporting suspicious activity quickly and following security best practices greatly increases the likelihood of recovering lost funds.

Useful links

We’ve discussed a lot in this guide, but there might still be more you want to discover about fraud detection. Browse these handy sources to learn more.